Weekly Bulletin #19

Market Valuation & Recessionary Rhymes | Essentra Plc | High Yield Credit Spreads

Disclaimer

Value Situations is NOT investment advice and the author is not an investment advisor.

All content on this website and in the newsletter, and all other communication and correspondence from its author, is for informational and educational purposes only and should not in any circumstances, whether express or implied, be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

Market Valuation & Recessionary Rhymes

There are recurring cycles, ups and downs, but the course of events is essentially the same, with small variations. It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes.

Theodor Reik, The Unreachables (1965)

The above adage, often condensed as “History doesn’t repeat itself, but it does rhyme” and attributed to Mark Twain, seems particularly apt to me in the context of the current market environment, with growing fears of a recession driven by inflation concerns, rising interest rates and slowing global growth.

Against this backdrop, there are rising expectations that US corporate earnings will start to contract as margins become squeezed in a looming recession. Certainly when looking at how far corporate profit margins are above their long-term average levels, some kind of mean reversion seems plausible, if not highly probable, given the macro forces at play:

Historic Operating and Net Profit Margins for the S&P 500 Index (SPX)

Source: S&P Dow Jones Indices; Value Situations analysis.

The chart above shows how the SPX’s current operating margin of 13.4% and net margin of 12.7% are both well above their respective long-term averages of 8.7% and 7.5%; in fact on both measures, the SPX’s margins are at all-time highs. I’m also reminded here of something GMO’s Jeremy Grantham once said with respect to profit margins:

Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism.

Certainly the combination of slowing growth, a protracted war in Ukraine, de-globalisation, rising interest rates and high inflation all occurring simultaneously seem a likely catalyst for a recession and mean reversion in profit margins.

Yet this doesn’t appear to be priced into stocks currently. The SPX is currently trading at ~19.3x LTM EPS (based on net reported EPS), which on a headline basis may not seem problematic, being below the index’s historic average multiple of ~26x over the last ~25 years (I’m arbitrarily assuming here that the last 25 years is an appropriate historic timeframe for comparison on the basis that is representative of the modern, post-internet, tech-driven economy). But remember that this 19.3x multiple reflects recent all-time high profit margins, and so perhaps reflects a cyclical peak.

What if margins were to mean revert closer to the historic average of ~7.5%, given cost inflation, lower growth and higher interest costs for corporates? Assuming sales at the index level stay flat, and margins mean revert due to the forces outlined above, this would imply the SPX is trading at 32.5x today on a forward basis (+25% above its historic average). But it is perhaps a little optimistic to assume that sales flatline in a recessionary environment and given the macro forces at play. So lets assume SPX aggregate revenues decline ~10% as they did at the dotcom market trough in 2002, and margins revert to historic mean levels; this would imply a forward multiple of ~36x for the SPX today. Furthermore, if we assume SPX revenues were to decline ~15% as they did at the GFC trough in 2009, the implied multiple rises further to ~38x. On this basis, it would appear that the market is yet to adequately price in the potential margin contraction amid the known and growing recession risks. This suggests stocks at the index level remain overvalued and potentially have much further to fall, despite the recent 20% bear market correction.

This also prompts the question of what might the stock market impact be of a recession and a decline in corporate earnings? Would the stock market reaction rhyme with the 2000-2002 dotcom crash or 2007-2009 subprime bust? My own sense is that the current experience rhymes more with the dotcom bubble, with some clear parallels:

The dotcom crash followed a speculative mania in tech stocks, and specifically in unprofitable and even pre-revenue internet-related stocks as mass adoption and growth of the internet occurred; this rhymes with the growth/innovation tech bubble that started to burst towards the end of last year, led by names such as Peloton (PTON), Carvana (CVNA), and the Ark Innovation Trust (ARKK), as well as the collapse in cryptocurrencies such as bitcoin and NFTs.

The dotcom era was also marked by a flood of failed IPOs of companies with highly questionable (or non-viable) business models, which rhymes with the SPAC bubble that burst earlier this year.

The recent surge in retail investment, particularly in meme stocks such as GameStop and AMC is also reminiscent of the retail investing boom in internet stocks during the height of the dotcom bubble.

The 9/11 attacks and subsequent “War on Terror” that commenced in late 2001, after the dotcom bubble peak, but before the market trough some ~12 months later, represented a significant shift in the global security order; Russia’s invasion of Ukraine earlier this year rhymes with the 9/11 aftermath in that it too represents another shift in the global security and political order.

In contrast to the dotcom crash, the GFC was a credit-liquidity crunch that evolved into a global banking and financial crisis, the conditions for which don’t really exist today given that the banking system is more regulated and banks are generally better capitalised. In that context and given the parallels (or rhyming conditions) outlined above, the dotcom bust seems like the more appropriate analogue to today’s market if we are to believe a recession and market decline is to occur from here. As such, a comparison of the dotcom bubble and aftermath to today’s market may provide an interesting guide as to what could unfold in the months ahead.

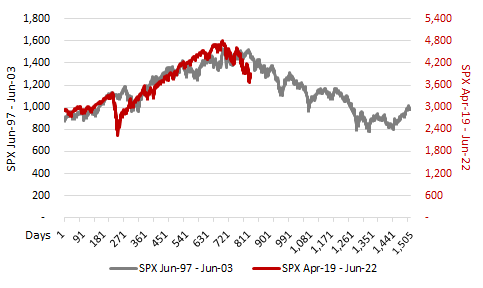

Interestingly, overlaying the SPX’s rise to its most market peak (and all-time high) reached in January of this year against the dotcom market trajectory to its March 2000 peak maps very close to an exact fit as shown in the chart below, and implies a significant further and protracted decline for the SPX over the next ~18 months if a similar market trajectory is to play out:

Source: Value Situations analysis; Koyfin.

In the dotcom collapse, the SPX declined -49% from peak to trough over a period of 929 days. The SPX currently sits at ~3,918, or -20.4% below its all-time closing peak of 4,796.56 reached on 3 January this year. A repeat of the dotcom experience (a similar 49% drawdown from the Jan-22 peak) implies the SPX would decline a further -38% before bottoming at ~2,400 by November 2023.

To be clear, none of this is intended as a prediction - I am comfortable admitting that I do not know what way the market will go, but I do think this is an interesting thought exercise given current recessionary concerns, the known market risks and the obvious parallels between the dotcom era and the recent speculative tech/crypto bubble.

The main takeaway from this exercise for me is that it indicates market risk remains elevated, valuations are still high and the potential for a significant drawdown is real. In that light, and with inflation running at ~40 year highs, this leads me to conclude that selected equity investments in overlooked, niche assets outside the main indices, constrained-supply commodity situations and special situations (such as recent Value Sits ideas SOL Group and Alphamin Resources) are the most interesting pockets of the market to look for ideas in the current environment.

Essentra Plc

Previous Quick Idea name Essentra Plc (ESNT) last week announced it has agreed to sell its Packaging division to Austrian packaging group Mayr-Melnhof Group for £312m on a debt free/cash free basis, or 12.4x EBITDA. This is well ahead of my previous estimate of £210m for the division based on my assumed ~9x multiple and is an excellent outcome for ESNT as it pursues its strategy to become a pure play industrial components business.

ESNT’s share price has declined ~20% since I wrote about it last December, reflecting cost inflation concerns and most recently recessionary fears. Following this disposal , and assuming it completes the intended disposal of its Filters business at a 9x multiple as outlined in my previous analysis, I estimate ESNT will realise total cash of ~£590m from the two divestments, which will transition the balance sheet to a net cash position. This would transform ESNT into a more focused, pure play components business valued at just 6.4x on a PF basis at the current current share price (vs. 12x -13x average NTM multiple for peers). A re-rate in line with peers indicates upside of ~70% to ~£4.40/share, implying a return profile of ~30% IRR / 1.7x MOIC over a two year investment term from here.

As a break-up/value story with limited analyst coverage, I continue to view ESNT as an interesting, event-driven situation that is worth monitoring, with a successful disposal of the Filters business being the critical next step.

Any Other Business

For this week’s AOB I’m sharing Trey Lockerbie’s excellent interview with Dan Rasmussen, Founder and Portfolio Manager of Verdad Advisors on the We Study Billionaires Podcast.

As readers of this newsletter will know, the current widening of high yield credit spreads is a topic of interest to me and a potential basis for concern (being an indicator of tightening liquidity and worsening economic conditions). In this podcast discussion, Rasmussen discusses how he uses the high yield spread to determine the current macro environment and I believe this is a timely discussion given the current macro backdrop.

Why Not Subscribe to the Paid Tier?

If you find the ideas in this newsletter interesting, please considering signing up to the newly launched Paid Tier.

You can read more about the paid offering here.

This newsletter is 100% reader supported and free from conflicts of interest or other commercial considerations. In writing Value Situations my job is essentially to generate ideas for subscribers that supplements their own idea origination process.

Furthermore, I believe the value proposition for paying subscribers is compelling. I am a former private equity/special sits investor that has worked with one of the largest alternative investment firms in the world, and so paying subscribers will be getting thoughtful, buy-side quality ideas and analysis for a very small fraction of the cost of employing a buy-side analyst full-time.

If you find this newsletter interesting, please also consider sharing it with friends and colleagues by clicking the Share button below.

Here’s what other investors are saying about Value Situations:

Value Situations was named as one of the Top 100 Must Follow Stock Research accounts by Edwin Dorsey of The Bear Cave Newsletter:

Great analysis Conor to put into context a possible margin contraction.

I believe that in this first part of the correction what we are seeing is a compression of multiples due to the irrationality of the valuations that were paid. In the next few quarters it is possible that the additional correction will come from the fall in profits and the decline in margins.