The Arithmetic of Asymmetry

The benefits of an asymmetric risk/return criterion for picking stocks

Disclaimer

Value Situations is NOT investment advice and the author is not an investment advisor.

All content on this website and in the newsletter, and all other communication and correspondence from its author, is for informational and educational purposes only and should not in any circumstances, whether express or implied, be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

The goal in investing is asymmetry: to expose yourself to return in a way that doesn’t expose you commensurately to risk, and to participate in gains when the market rises to a greater extent than you participate in losses when it falls. But that doesn’t mean the avoidance of all losses is a reasonable objective. Take another look at the goal of asymmetry set out above: it talks about achieving a preponderance of gain over loss, not avoiding all chance of loss.

Howard Marks

In this this week’s newsletter I want to discuss a key part of my analytical framework in further detail, prompted by a question from a subscriber who emailed me last week asking why I place such importance on it.

With the future inherently unknowable, risk is inherent to investing. Things can, and do go wrong despite the best research, due diligence and analysis, and this holds true for all investors. In making an investment, one implicitly accepts the possibility of things not working out and incurring a loss. Even if you buy a stock with firm conviction, you are still “signing up” for the possibility that you could lose some or all of your investment. The trick is to mitigate this risk by finding situations where this risk has been mispriced in the market, and exploiting this mispricing.

With this in mind, my asymmetry requirement helps me tilt the odds of success in my favour. While I consider myself a fundamental value analyst, I came to understand this concept of asymmetric investing in reading about two leading macro investors, Paul Tudor Jones and Stanley Druckenmiller.

In his book Money Master The Game self-help performance coach Tony Robbins explained how Jones (a client of his) uses asymmetric risk/reward to guide his investment decisions. In simple terms, Jones seeks out 5:1 investments, where for every $1 that he puts at risk in an investment, he believes he can make $5 in return. Jones employs this framework as he knows that he’s going to be wrong many times in his investing. As Robbins explains:

Jones is willing to risk $1 million when his research shows he’s likely to make $5 million. Of course, he could be wrong. But if he uses the same 5:1 formula on his next investment, and he’s successful, he will have made $5 million, minus the first investment loss of $1 million, for a net investment gain of $4 million.

Using this formula of constantly investing where he has the opportunity for asymmetric rewards for the risk he’s taking, Paul could be wrong four out of five times and break even. If he loses $1 million four times in a row trying to make $5 million, he’ll have lost a total of $4 million. But when the fifth decision is a success, with a single home run he’s earned back his total $5 million investment.

Breaking out the math with a simple example here is helpful in demonstrating the effectiveness of Jones’ asymmetric approach. If he is wrong 4 out of 5 times, and successfully hits a 5x return on his fifth investment he breaks even:

If he is correct with only two of his 5 investments, he still doubles his money overall, despite having been wiped out completely with his first three investments:

While this simple example elegantly demonstrates the power of an asymmetric risk/reward approach, it does rest on one very big assumption - it assumes one can find opportunities that can deliver 5x returns in the first instance. In my experience, finding a double is difficult, never mind finding 5 potential 5-baggers!

Of course, in the context of Jones’ global macro style of investing, 5x type risk-reward opportunities are perhaps easier to find compared with public equities, given the extensive use of leverage and derivatives in global macro. Nevertheless, I believe an asymmetric risk/reward framework fits with Warren Buffett’s famous rules of investing in a fundamental value context:

Rule No. 1: never lose money; rule No. 2: don’t forget rule No. 1.

Applying an asymmetric risk/reward approach to a fundamental equity strategy actually reinforces Buffett’s rule of preserving capital. Stanley Druckenmiller is another investor who has employed an asymmetric risk/return framework to great success. He has said that “the way to build long-term returns is through preservation of capital and home runs” and Druckenmiller has clearly achieved this in his own career via asymmetric investment situations. He expanded on this, stating that of the lessons he’s learned from his former boss George Soros, “perhaps the most significant is that it’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.” This outcome is maximised by insisting on asymmetric return profiles for every investment.

Druckenmiller’s track record of compounding his investors’ capital at over 30% p.a. for over 30 years while never having a down year clearly indicates that his asymmetric framework works. Furthermore, I believe this framework can be applied to public equities by assembling a basket or portfolio of names with asymmetric risk/reward profiles, which should lead to above average returns over time.

The following thought exercise demonstrates how I think about applying this asymmetric framework to fundamental equity investing. Firstly, let’s say I select 10 names over the course of a year that I believe are actionable and offer up to ~100% upside over a 2-3 year investment horizon, such as Dole Plc and Dalata Hotel Group.

In my risk/reward framework, I’m typically willing to accept up to ~30% downside risk in a worst case (which I also deem to have a low probability of occurring given my assessment of key risks and corresponding mitigants). So if I’m just plain wrong in my analysis of a given situation, the maximum loss I expect is approximately a third of the entry price. So I’m essentially shooting for situations with asymmetric return-to-risk profiles of 3x (~100% upside being ~3x downside risk in the low 30% range).

Next let’s assume I construct the basket of equities with equal weighting across the 10 names. I typically underwrite with a 2-3 year timeframe, within which I expect my estimate of target value to be realised based on identified catalysts. For the purpose of this exercise I’m going to assume a 2.5 year investment term, being the midpoint.

While I have conviction in the names I underwrite, I have to accept that I will be wrong on some of them. Let’s assume I will be wrong 50% of the time. This is where the benefit of an asymmetric framework becomes evident. Even at a 50% hit rate, a portfolio of names that offer the type of asymmetry I seek should still outperform the general stock market over time. This is due to the the arithmetic of asymmetry, which I set out below.

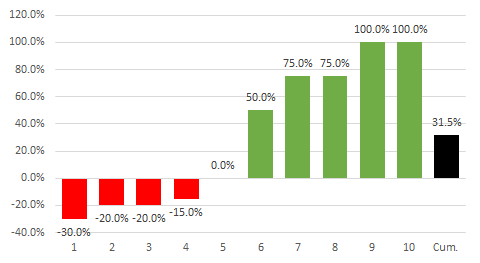

In terms of outcomes, lets assume that despite all my work in finding and analysing these equities AND after factoring in what I believe to be honest downside assessments with solid mitigants, I’m proven wrong on 5 out of the 10 names. Let’s assume here that of the stocks selected, 5 lose money or do nothing (the “Losers”) and the other 5 play out well, to varying degrees (the “Winners”).

This range of outcomes might look as follows:

The Losers:

1 name loses 30%

2 names lose 20%

1 name loses 15%

1 name does nothing, and stays flat

The Winners:

2 of the 10 names double, returning 100%

2 names return 75%

1 returns 50%

This outcome implies a cumulative return across the basket of +31.5%, distributed across each position as follows:

So despite only a 50% hit rate, the basket is up overall on an absolute return basis, with an implied return profile of 11.6% IRR / 1.32x MOIC over 2.5 years. Not stellar returns, but acceptable and crucially Buffett’s Rule #1 has not been violated, despite a 50% fail rate.

Of course, the above exercise is a theoretical one and clearly rests on assumptions that are open to question, the obvious one being what if I’m really unlucky (or plain wrong) and 9 or even all the names selected are duds, and lose 50% or more ? It’s possible of course, but what I would say in this regard is that each of the 10 names selected represent well researched, high conviction ideas (such as Dole or Dalata) where a worst case outcome of up to a -30% loss is assessed as a low probability outcome given (1) the positive investment characteristics and risk mitigants underpinning each underwrite and (2) the plausible catalysts for re-rating identified in each instance. On this basis, I think it’s reasonable to expect that 5 of the 10 names would work out well.

While I am focused on absolute rather than relative returns, the returns implied by this asymmetric framework also outperform the average return one should expect from the stock market over time.

Since 1990, the S&P 500 has returned ~8.6% per annum, while the European Stoxx 600 has returned 5.6% over the same period. Given that the focus of Value Situations is on US and European equities, an appropriate benchmark for relative performance assessment in this example might be a 50/50 blended average of the two indices. On this basis, the simple average return for US and European equities is ~7%, which my theoretical basket above outperforms by a healthy 4.6%.

Again I’m aware this comparison is open to question, and assumes my asymmetric basket can be refilled every 2-3 years with 10 or so names with asymmetric risk/return profiles that achieve similar results to the above example. But that’s the job of the full-time investor/analyst – to protect capital and earn an acceptable rate of absolute return, which should really be above the market rate of return otherwise he or she is better off just buying a low cost index fund or ETF.

In the current market, overlooked and out-of-favour sectors such as real estate and energy are areas where I see the potential for asymmetric returns, particularly where there is a supply/demand imbalance and a possible inflationary tailwind, with uranium being a very interesting current example in this context.

In conclusion, I believe an asymmetric framework is essential to protecting capital and achieving above average returns over time, as it skews the odds of success in my favour and increases the probability for absolute and outsized returns.

In presumptive theory - totally plausible.

Would've liked to see some picks where this formula has been applied and proven successful.