A Hot Desk Bet

Opportunities from structural change and the new normal for offices

Welcome to the third issue of Value Situations, and the second of the regular weekly “quick ideas” editions. In this issue, I discuss looking for opportunities in areas of the market undergoing structural change and an interesting play on the post-COVID office market that may offer compelling upside as cities re-open and workers return to a new approach to office working.

Disclaimer

Value Situations is NOT investment advice and the author is not an investment advisor.

All content on this website and in the newsletter, and all other communication and correspondence from its author, is for informational and educational purposes only and should not in any circumstances, whether express or implied, be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

Structural Change as a Source of Opportunity

In discussing the search for new investment opportunities in his Q2 2014 letter to Baupost investors, Seth Klarman emphasised creativity in the investment process, writing “Our analysts are doing some really creative work thinking about structural changes in some companies and industries, which has led to several new public equity investments.” As I’ve mentioned previously, I believe creative thinking is an important skill in finding new and original investment ideas.

Klarman makes an interesting point regarding companies and industries undergoing structural change as a source of opportunity. Structural changes can be broad-based across an industry, such as disruptive technology or trends (Netflix, streaming and cord-cutting), or idiosyncratic situations such as corporate re-organisations (bankruptcy exits, mergers) or changes in business models (e.g. shift from software licence to SaaS models).

From Klarman’s letter, Baupost’s 2014 investment in memory and data storage chip manufacturer Micron Technology makes a good case study in this regard. Micron was one of a number of players in the volatile memory chip industry, which started to undergo consolidation from 2012 to counteract a boom-and-bust cycle characterised by oversupply and a resulting plunge in chip prices. Micron acquired Japanese peer Elpida, a leading supplier of chips to Apple, out of bankruptcy in 2012, while Micron itself had been intermittently loss-making up to that point. The Elpida deal transformed Micron from the #4 player to the second largest in the industry behind Samsung. Furthermore this structural change to Micron at the corporate level occurred against the backdrop of structural change across the industry with consolidation among other chip manufacturers and with the secular tailwind of smart phones and mobile computing leading to a boom in demand for memory chips. In the two years following the Elpida acquisition, Micron’s stock went up approximately 5x, illustrating the power of catching a structural change catalyst.

So how we can use this fishing rod of “structural change” in the choppy waters of today’s equity market?

The Changing Office Market

Post-COVID, offices are perhaps the one sector undergoing the most pronounced change following the great remote work experiment necessitated by the pandemic. COVID accelerated an acceptance of home or remote working arrangements globally, and it’s now acknowledged that remote work is here to stay in some form. As such, the office’s position as the primary place of corporate work will need to evolve. While we don’t yet know exactly what future work practices will look like, one thing is clear - the format and purpose of the office is changing.

There are two broad schools of thought as to the future of the office. On the one hand, there is a view that remote working or working from home (WFH) will gradually displace the office as the primary work location across most industries, rendering the traditional office as we know it dead, possibly akin to the retail apocalypse for malls and traditional retail. This view quickly emerged during the early stages of COVID lockdowns when there was a rush among commentators to appear prescient and proclaim the death of the office on the basis that productivity levels appeared to hold up while workers enjoyed the benefits of more time at home and avoiding long commutes. Furthermore, the apparent success of WFH was viewed as an opportunity for corporate office downsizing and cost savings. This narrative most clearly manifested itself in the steep discounts suffered by prime office REITs during the depths of the lockdowns, which traded as low as ~0.5x - 0.6x NAV vs. their previously reliable 1x+ levels.

Indeed, this initial narrative didn’t just stop at proclaiming the office is dead, but went even further to declare the city itself was dead. Of course, this was an incomplete take and perhaps the most extreme form of recency bias; while cities such as London and New York did hollow out as young workers left to be closer to parents and families, much of this now appears temporary, with evidence that many workers want to return to city offices again for career advancement. Furthermore, while much has been made of workers with young families departing to lower cost/lower density locations, it seems to have been overlooked that many moved to .… other CITIES; in the case of New York, workers relocated to cities such as Miami, Dallas and Phoenix, to work from a mix of home offices and nearby hybrid or satellite offices. This suggests that the office remains relevant, albeit it an evolving, re-positioned format.

The second line of thought is a “new normal” hybrid model involving both in-office work and some degree of flexible WFH arrangements. While this will vary across industries and organisations, it is expected that traditional city offices will evolve rather than become obsolete, being destination buildings or campuses suited to the post-COVID environment, with features such as reconfigured desk lay-outs, superior ventilation and greater collaboration space rather than just offering high-density, desk-led accommodation. This to me seems the most likely outcome for a number of reasons.

Productivity – during the early phase of WFH in lockdown, worker productivity was maintained and even improved in some instances but this now appears to be illusory; when the lockdowns hit in March 2020, many corporates’ H1 2020 business pipelines in sectors such as tech and professional services had been filled pre-lockdown and so projects were delivered without any apparent disruption to output. From speaking with contacts in various industries during Q1 this year, the same cannot be said for H1 2021 – as lockdowns were re-introduced again in January as COVID cases surged, new business proved difficult to win and productivity reduced dramatically, prompting increased corporate statements regarding retaining offices and returning to them (discussed below).

Social Interaction & Collaboration - Real estate entrepreneur Sam Zell has highlighted how humans are social animals and corporate culture cannot be maintained remotely - “you can’t motivate by modem” or “evaluate performance through a screen” as he summarised this point. Remote working has proven it is very difficult to manage teams, train and mentor employees, and communication and interaction is much less efficient also. It’s therefore reasonable to conclude that an organisation needs a central, regular meeting hub to function properly.

Health & Wellness – it’s been well documented that employee mental health has been adversely impacted by remote working, with the blurring of work and home boundaries leading to exhaustion from longer work hours, the lack of social interaction, and “Zoom fatigue.” A recent Stanford University study found increased stress levels as a result of frequent and lengthy video calls replacing in-person meetings. A quality office hub would clearly address this real issue.

Economic Necessity– a key point that I don’t see mentioned is the extremely negative impact to national economies of a decline in city office usage. We have already seen how a significant shift to WFH resulted in the hollowing out of city centres and shutting of small businesses such as shops and restaurants. It’s also a fact that cities are the engines of national economies and a few simple statistics make this starkly evident – Greater London accounts for ~24% of UK GDP, the Paris region accounts for ~31% of France’s GDP, while in the United States New York City, Los Angeles and San Francisco combined account for ~16% of US GDP (St. Louis Fed data). So there’s an obvious economic imperative here for governments to prevent the decline of cities - national economies simply cannot afford for their engines to become muffled, particularly given the soaring public debt borrowed to combat the pandemic. Furthermore, suburbs and secondary cities are not set-up to absorb a diaspora of city office workers, and such a migration would create wider social and economic issues for years to come. Therefore I see a clear political incentive to stimulate and revive urban centres post-COVID, which is supportive of the office market.

Human Nature – Since Uruk was established as the first great city in ancient Mesopotamia in the third millennium, humans have congregated and settled in cities to trade, socialise, learn and advance civilisation. To believe the office is dead is to believe cities will remain empty, which in turn implicitly assumes a fundamental reversal in how humans interact and how civilisation has functioned for millennia. I just don’t see how a 15 month pandemic for which there is now a vaccine is powerful enough to effect such societal change.

One final thought worth remembering is that after the September 11th terrorist attacks of 2001, many commentators predicted high rise office buildings were defunct and people would not work in them again for fear of further terrorist attacks. What followed was a boom in New York office development culminating in the rebuilding of the World Trade Centre site. Rather than a decline in office development and attendance, what actually happened was improved, more robust building design and heightened airline security. Humanity adapted and continued on rather than reversing course.

All the above factors suggest that the city office will remain the primary work location, and this is starting to ring true based on recent statements from corporate employers, whose tone has noticeably changed from 12 months ago:

Barclays CEO Jes Staley now expects staff to return to the office, stating that home working is not sustainable, despite having previously said city offices were a thing of the past during the depths of the lockdown last year

Similarly Goldman Sachs and JP Morgan have both called an end to remote working and require all staff back in the office

Amazon are offering a hybrid work model, with a mix of working between the office and home, with a baseline of 3 days a week in the office as part of a return to an “office-centric” culture as their “baseline”

Google are investing $1bn+ in new offices post-COVID to support their corporate culture and collaboration

Tellingly, a recent KPMG survey of over 500 CEOs supports a return to the office as being the likely post-COVID outcome, with only 17% of executives surveyed looking to downsize their office requirement (vs. 69% when surveyed in August 2020), while only 30% are considering a hybrid model with a mix of office-based work and WFH 2-3 days per week for staff.

This indicates that while WFH will be a feature of future work practices, the core office will remain the primary place of work. It is more likely (generally speaking across industries) that flexible WFH arrangements will be the latest corporate perk to attract staff, following on from previous benefits such as health insurance, staff canteens and on-site gyms.

It now seems that the office market is on the cusp of structural change in terms of how offices will be used and designed in the future, with a “Great Reconfiguration” coming as the vaccine roll-out completes and workers return. Indeed the latest soundings from the industry suggest that reconfiguration of existing office space is the priority for the market now – according to a recent survey from Unispace, ~30% of companies surveyed across the Americas and EMEA regions are looking to develop new space or completely reimagine existing environments, with “most focused on reworking and reconfiguring their current offices to support post-Covid ways of working.” Similarly, CBRE stated in their most recent earnings release that “the configuration of offices will change, and that'll create some real opportunity for us to do work for our clients.” Furthermore, this idea of re-design of office space is starting to show through in the latest data, with leading office furniture manufacturer Steelcase reporting that orders are up 25% Q-o-Q in its most recent quarterly results, with a significant increase in customer visits, product mock-ups and requests for proposals during the quarter as companies plan for their employees to return to the office.

It is now evident that the post-COVID return to the office represents perhaps the greatest overhaul of office design and usage since the “cubicle farms” of the 1980’s, and will involve not just extensive reconfiguration of existing office space but will also impact the design of all future office development.

So how does one play this structural change in the office market within public equities?

Herman Miller – A Changing Company in a Changing Market

While the most obvious play may be to look for fundamentally undervalued office REITs (such as Hibernia REIT), given this prospect of a Great Reconfiguration, I believe the office furniture sector could also provide real upside leverage to the future of the office theme.

Regardless of how the office evolves post-COVID, office furniture manufacturers should benefit from BOTH the return to the office and new remote working practices; existing and new-build offices will require new furniture fit-outs to meet post-COVID design requirements, while the increase in WFH will mean the home office becomes a purpose built and furnished workspace rather than the improvised bedroom or kitchen table “office” necessitated by the lockdowns during the pandemic.

This suggests that office furniture specialists should see a significant increase in demand over the next 2-3 years as both companies and homeowners overhaul their workspaces.

Of the major office furniture manufacturers, Herman Miller (Ticker: MLHR) looks the most interesting in this context. MLHR is the #2 player in the office furniture industry by revenues ($2.3bn in FY20) behind Steelcase (SCS, with $2.6n of revenue). In April this year, MLHR announced it was acquiring the #5 player Knoll (KNL) for $1.8bn (~14x LTM EBITDA, or ~8x including synergies).

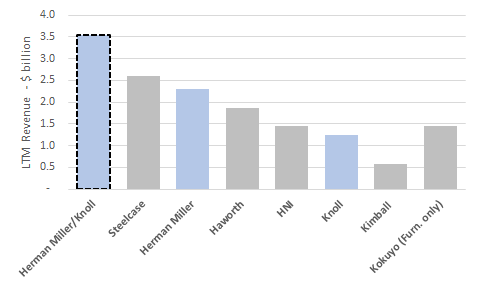

The deal is a transformative one for both MLHR and the industry, as it changes the competitive landscape, making the combined MLHR/KNL business the market leader ahead of Steelcase with PF revenues of ~$3.6bn:

Source: Herman Miller + Knoll Presentation, April 2021

Of the peer group, Steelcase, HNI and Kokuyo are publicly traded and Haworth is privately held. Kokuyo is less directly to MLRH/KNL as it is a Japanese-listed manufacturer of office supplies and furniture – the above shows its office furniture segment revenues only which are ~44% of its total revenues.

What I like about the MLHR/KNL situation is that it capitalises on structural change at both the industry and company levels – MLHR will benefit from both the office reconfiguration and remote working shifts, and from a strengthened position as the market leader with competitive advantages of enhanced scale and product offering.

Post-acquisition of Knoll, MLHR will be a US commercial office-focused business, with ~75% of PF revenue from the US market and ~80% from the commercial office segment:

Source: Herman Miller + Knoll Presentation, April 2021

However, what is perhaps not fully appreciated is how MLHR will be particularly well positioned to capitalise on the remote working/WFH trend as a result of the deal. Historically, office furnishings have been separated from home furnishings, but this deal will push MLHR directly into the hybrid residential-commercial niche of the home office - the combined residential revenues of MLHR/KNL will be ~$700 million, making it the third largest residential/retail furniture provider on industry journal Furniture Today’s Top 25 list.

Deal Summary

MLHR is acquiring KNL in a stock and cash deal with a total EV of ~$1.8bn or ~14x LTM EBITDA (~8x including expected synergies).

KNL shareholders will receive $11.00 in cash and 0.32 shares of MLHR stock for each share of KNL stock owned. Based on MLHR’s current share price of ~$48, this implies a purchase price of $26.36 per KNL share or a ~53% premium to KNL’s closing price pre-transaction announcement. Upon completion, MLHR shareholders will own ~78% of the combined company and KNL shareholders will own remaining ~22%. The deal also involves MLHR acquiring PE firm Investindustrial’s preference shareholding in KNL for a fixed price of $253m. The deal is expected to close in Q3 2021

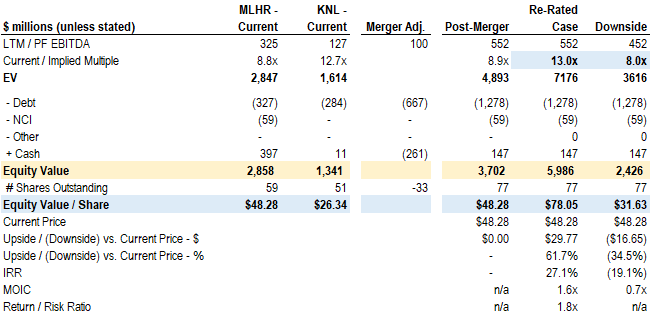

Valuation Analysis

At the current MLHR share price of ~$48/share, the combined MLHR/KNL entity is valued at ~9x PF EBITDA (including synergies), which compares to ~12x – 13x NTM EBITDA for MLHR/KNL’s three US-listed peers (Steelcase, HNI and Kimball).

Applying a 13x peer group multiple to MLHR/KNL’s PF EBITDA implies a share price of $78/share for the combined business, or ~62% upside to the current share price:

Source: Value Situations analysis

The above summary analysis gives credit to the expected $100m in cost synergies to be achieved over two years, which I think is reasonable given how complementary the two businesses are and the degree of overlap around areas such as supply chain, procurement and logistics.

MLHR’s net leverage will increase to ~2x as part of the deal, as it has secured $1.75bn in committed debt financing from Goldman Sachs to support the acquisition, comprising $1.25bn in senior term loan facilities and a $0.5bn revolver which is not expected to draw on closing of the deal.

MLHR’s share count will also increase, from 59m to ~77m shares outstanding reflecting the dilution from the share consideration paid to KNL shareholders.

A 13x NTM multiple seems justifiable as the $552m is LTM EBITDA plus cost savings, and so doesn’t reflect any future revenue and earnings growth. Additionally, MLHR’s PF EBITDA margin of ~16% compares very strongly to peers’ margin range of ~8% - 10%. Given the growth prospects, market leading position and superior margins MLHR merits a multiple at the higher end of the peer range.

For an indicative downside, if one assumes none of the synergies are achieved (a pretty unlikely outcome given the overlap and similarity of operations) and a static 8x multiple based on MLHR’s average multiple over the last three years, the implied downside is -35% from the current share price, indicating a reasonably asymmetric return profile of close to 2x upside vs. downside risk. Based on a two year investment term (in line with the two year time frame expected to achieve full cost synergies) the indicative return profile is ~27% IRR / 1.6x MOIC.

While the deal still needs to be approved by both sets of shareholders and obtain necessary regulatory approvals, completion risk appears low - both boards have approved the deal, while KNL’s pref shareholders Investindustrial have also pre-approved it, the value creation opportunity should appeal to MLHR shareholders, while the 50% premium is compelling for KNL shareholders. On the regulatory side, although the combination creates the largest player in the market, this isn’t of a scale that would run into competition issues given a total market size of ~$71bn, and given some competition from non-office furniture players sector such as Restoration Hardware, Wayfair and Williams-Sonoma.

At the current implied ~9x multiple, MLHR’s stock (even with the benefit of the imminent combination with KNL) is priced for no growth, despite it being clear that a new office cycle is commencing with the added growth tailwind of the residential/ WFH revenue opportunity.

The above is only a high level analysis, but when once considers how the structural changes happening in the office market support both a return to the office AND remote working, it seems the recent investor aversion to office-related stocks may be a case of recency bias rather than a full appreciation of the new outlook.

As such, I feel that office-related names may be mis-priced as we emerge from the pandemic, and are worth watching for value opportunities. Within this, MLHR appears to be one of the more interesting names to capitalise on this theme.

No idea how I came across this piece but some great points made about return to office. MLKN is incredibly cheap now.