2024 Model Portfolio Review

Model Portfolio return of +1.2% for 2024.

Disclaimer

Value Situations is NOT investment advice and the author is not an investment advisor.

All content on this website and in the newsletter, and all other communication and correspondence from its author, is for informational and educational purposes only and should not in any circumstances, whether express or implied, be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

I’m disappointed to report that following its strong performance in 2023 (+23.9%), the Value Sits Model Portfolio delivered an underwhelming performance in both relative and absolute terms for 2024, returning just +1.2% for the year, in line with reported performance at Q3-end, after flat performance for Q4.

For the year, the Model Portfolio trailed both of my preferred equity market benchmarks, namely the S&P 500 (SPX), by -22.1% (SPX +23.3% for 2024), and the European STOXX 600 (SXXP) by a less severe -4.8% (SXXP +6.0% for 2024).

Before getting into the drivers of Portfolio performance, it’s worth recapping briefly on what happened in equity markets last year, and what drove stock market performance generally. Reflecting back on 2024, there are stand-out three categories of outperformers that that come to mind:

Big Tech & AI;

Defence Stocks; and

Trump Trades

With regard to the first category, as I alluded to in my Q2 commentary the market’s performance in 2024 suggests that given current market structure (extreme concentration plus a short-term speculative/momentum focus) it seems almost impossible to match broad index performance, never mind beat it, without owning Nvidia (NVDA) or whatever the latest hype stock(s) may be.

The megacap tech stocks again led the way last year, with the Magnificent 7 cohort (now accounting for ~35% of the SPX) collectively appreciating ~63% in 2024, led by NVDA which rose ~171%. Indeed the “Mag7” were responsible for over half (~53%) of the SPX’s total return last year (although excluding the Mag7, the remaining SPX still returned a very solid 11.75%).

Looking beyond NVDA and the Mag7 cohort, in a perfect example of the market’s short-term momentum nature, certain utility names came to be regarded as second-order AI plays, allowing them to even outperform AI poster-child NVDA itself, notably Talen Energy and Vistra Corp:

Moving on to the second category of Defence stocks, these were another cohort that delivered strong outperformance last year, driven by an expected structural increase in defence spending supported by three interrelated factors:

Robust demand for weapons and ammunition arising from the ongoing war in Ukraine;

The growing acceptance that Europe needs to re-arm itself given the security threat now posed by Russia following its invasion of Ukraine; and

The re-election of Donald Trump and implications of this for NATO and defence spending generally in a more multipolar world facing security threats from Russia, China, Iran and others:

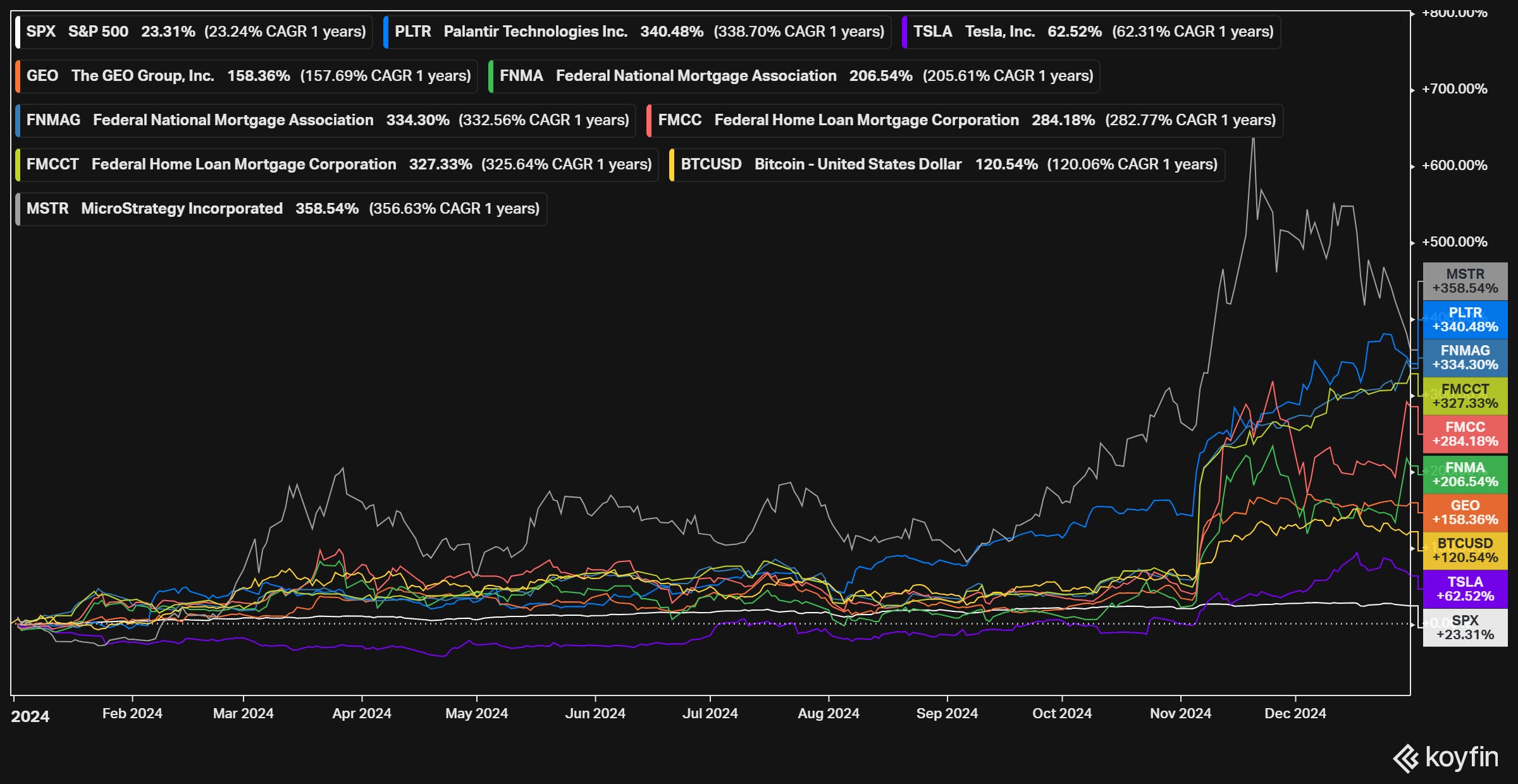

Finally, a miscellaneous and speculative collection of names that I collectively refer to as “Trump Trades” also outperformed significantly, with some names such as MicroStrategy, Palantir and the Federal National Mortgage Association outperforming the leading AI and defence names:

The chart above shows a broad section of names that were touted as “Trump” stocks in the run-up to the US election in November, and which subsequently performed very strongly into year-end, namely:

Bitcoin / MicroStrategy - a software company-turned-bitcoin play that rallied into year-end given the Trump administration’s expected support for bitcoin;

Palantir - a defence technology company whose largest client is the US government and founded by Peter Thiel, a Trump campaign supporter;

Federal National Mortgage Association / Federal Home Loan Mortgage Corporation (aka “Fannie Mae” and “Freddie Mac”) - two US government-sponsored mortgage financing companies that the Trump administration is expected to privatise, a trade currently being championed by Bill Ackman;

GEO Group - a for-profit prison operator that is expected to benefit from a clampdown on detention of illegal immigrants in the US; and

Tesla - perhaps the most obvious “Trump trade” of all, given Elon Musk’s support of the Trump campaign and his relationship with the pending administration.

This hindsight analysis suggests that to have beaten the market (as represented by the SPX) last year, one would have needed the conviction to bet on a mix of NVDA (again, after its ~239%+ gain in 2023!), seemingly arbitrary AI-electricity plays, European defence stocks (again, most of which had already appreciated significantly in 2023) and a hotpotch of stocks perceived as aligned with Trump or his allies. In summary, aside from perhaps some European defence names, I believe these winners were largely unpredictable at the start of the year and purely speculative in nature.

As I’ve written before, I’ve no interest in chasing momemtum in the hope of beating the market over a given 12 month period. After all such trades only work until they suddenly don’t, and typically come without any regard for valuation or downside protection. I much prefer to focus on undervalued and mispriced idiosyncratic situations with ample downside protection, as these offer superior, asymmetric returns over a reasonable timeframe.

On that note, let’s now delve into the Model Portfolio’s overall performance for last year…