Q2 2024 Model Portfolio Review

Portfolio return +1.2% YTD; exiting one position.

Disclaimer

Value Situations is NOT investment advice and the author is not an investment advisor.

All content on this website and in the newsletter, and all other communication and correspondence from its author, is for informational and educational purposes only and should not in any circumstances, whether express or implied, be considered to be advice of an investment, legal or any other nature. Please carry out your own research and due diligence.

Plus ça change, plus c’est la même chose.

Jean-Baptiste Alphonse Karr.

While the economic outlook and geopolitical conditions continue to evolve, it seems to be a case of the more things change, the more they stay the same for the US equity market and in particular with regard to AI darling stock Nvidia (NVDA).

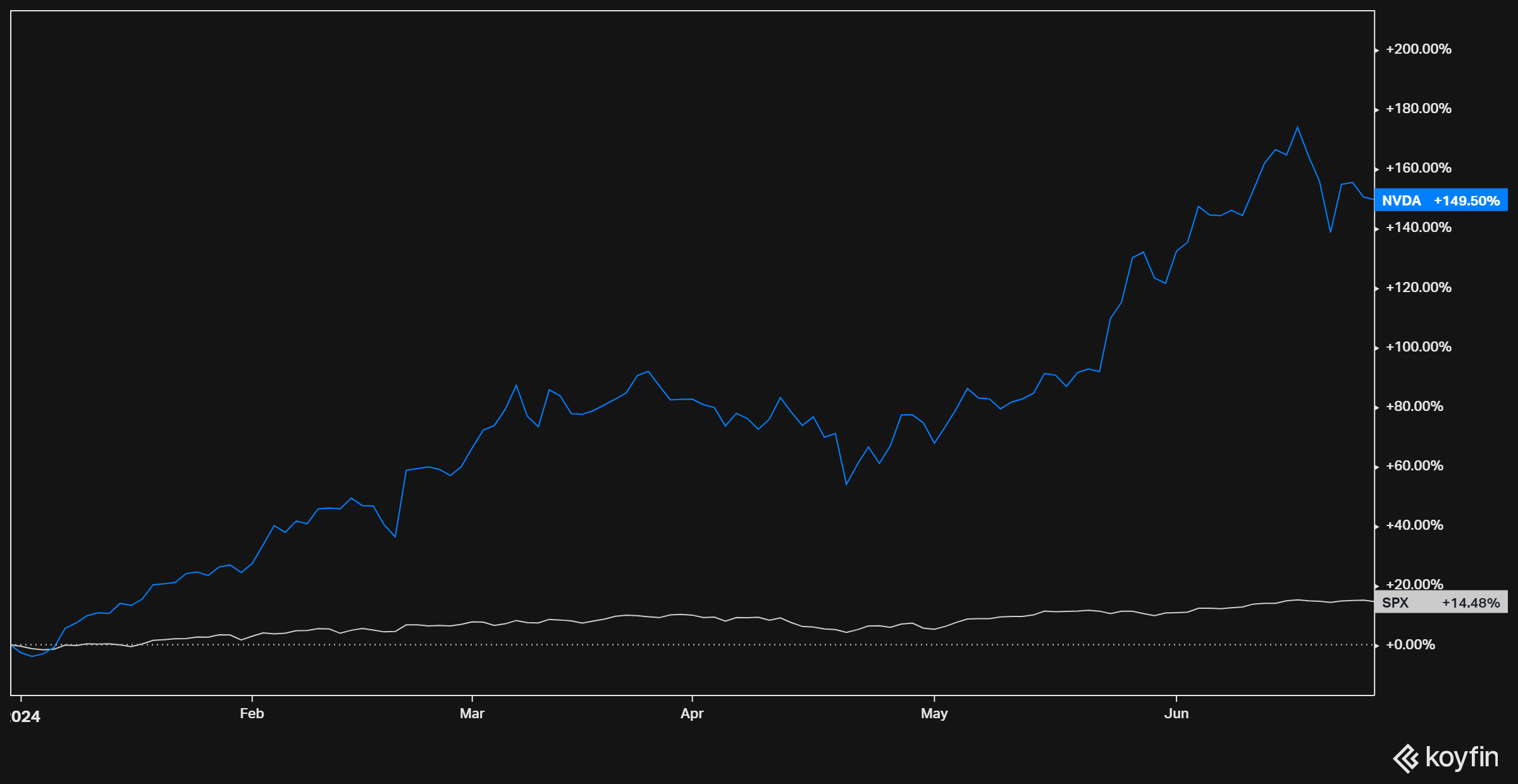

The lead story in markets for the first six months of this year has been NVDA’s continued surge, appreciating ~150% in H1, and that’s after a ~9% pullback since its high of ~$135+ in mid-June:

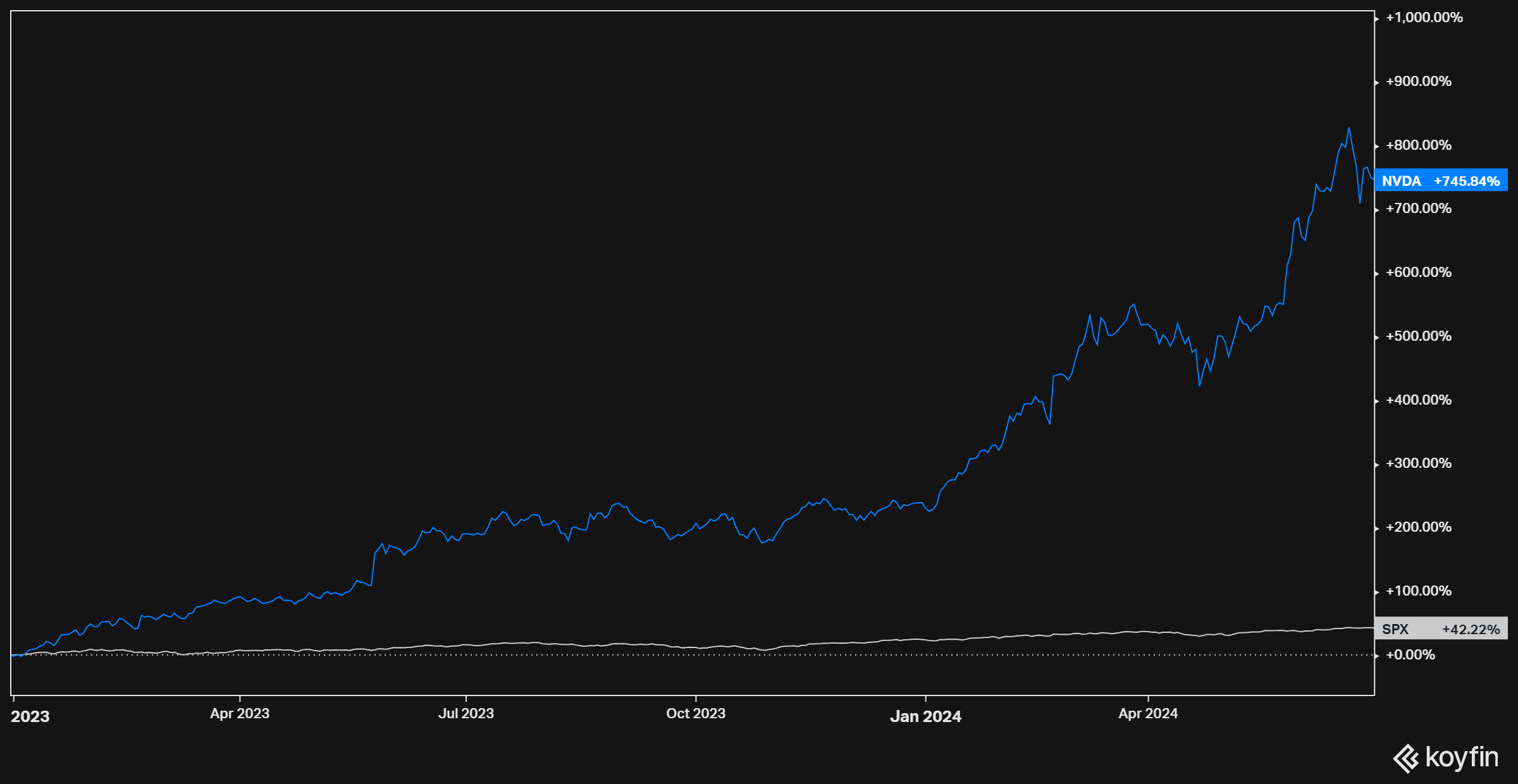

NVDA’s astonishing H1 performance sees it continue on its trajectory from last year, when it rose ~239% through 2023, and it is now up ~745% since the beginning of 2023 when AI became a whole new (and unforeseen) market-driving narrative:

NVDA now accounts for over 6% of the S&P 500 Index (SPX) but an incredible ~31% of its return YTD (of +14.5%), with the implication of this being that it is now almost impossible to beat the SPX benchmark without owning NVDA, or as one portfolio manager put it:

“We can’t keep up because we don’t own Nvidia,” said Max Wasserman, co-founder and senior portfolio manager at Miramar Capital. “If you don’t own that one stock, it really hurts. Every day feels like a root canal without novocaine.”

To give NVDA’s rise some additional context, at its mid-June peak it was more valuable than the entire stock market of France or that of the U.K., or the whole oil and gas industry. Such market dominance has also lead some commentators to declare that NVDA is now essentially carrying the carrying the US equity market.

This is a somewhat offhand summation and the reality is a little more nuanced, but it is not that far off the truth. More specifically, effectively five stocks drove the SPX to its ~14% gain for first half of 2024, namely NVDA, MSFT, AMZN, META and AAPL, which combined accounted for ~60% of the index’s gain YTD. Perhaps the more accurate story of H1-24 then is that the erstwhile Megacap 8 / Magnificent 7 club has essentially shrunk to five members now, which appreciated by an average of ~50% through H1-24 underpinned by their perceived potential to capitalise on the exponential growth promise of AI computing.

Such has been the dominance of these tech names that their performance has obscured that of the other 498 companies in the SPX (despite its moniker, the SPX actually comprises 503 companies at present). On an equal-weighted basis, the SPX appreciated just ~4% YTD, while if we were to exclude the “AI-5” above entirely from it, the index performance YTD would have been a more modest ~5.8%.

As I outline below, my Model Portfolio performed well short of the SPX no matter what way you cut it, with a return of just +1.2% for H1-24. This lacklustre performance combined with the lamentation of the portfolio manager quoted above might prompt me to question ask myself why not just follow the market’s lead and hold some NVDA and/or other AI-related names in an effort to catch up?

For me, the problem with owning something like NVDA now is that it is priced for perfection, at ~38x LTM sales and ~61x LTM EBITDA, and 25x and 39x on a NTM basis respectively. These NTM multiples imply a further +97% sales growth and +124% EBITDA growth YoY. This might seem somewhat plausible amid the current consensus view on AI’s exponential growth potential and the fact that NVDA grew sales and EBITDA by +126% and +498% respectively last year, but the risk of disappointment and a resulting severe drawdown just seems much too great here.

What happens if NVDA misses the consensus numbers underpinning its NTM multiples? In reality, the market is likely expecting NVDA to beat consensus levels (as it has in the past), and it is this beat expectation that is driving its current valuation, i.e. it will not be enough for NVDA to meet consensus estimates, it must surprise to the upside to justify its current market valuation.

Given such heightened expectations, any disappointment over actual performance 12 months from now is likely to disproportionately hit NVDA’s stock price to the downside, increasing the possibility of permanent capital loss, such is the level of frenzied optimism behind the name.

Given this risk, the lack of any real downside protection, and what I believe to be clear speculative fervour around NVDA and similar names, I much prefer to track and own cheap, idiosyncratic situations as I believe these offer better risk-adjusted returns via superior downside protection (e.g. asset backing) combined with strong upside potential supported by identifiable catalysts.

But enough about NVDA and AI, as the broader financial media already covers these in more detail than I ever could.

Now lets examine the Portfolio performance in further detail, beginning with a review of how the Portfolio was positioned at Q2-end, followed by a brief discussion of each position and one change to the Portfolio post-quarter end (made as of this morning).